7 / 132

7 / 132

05

EC World Real Estate Investment Trust ANNUAL REPORT 2016

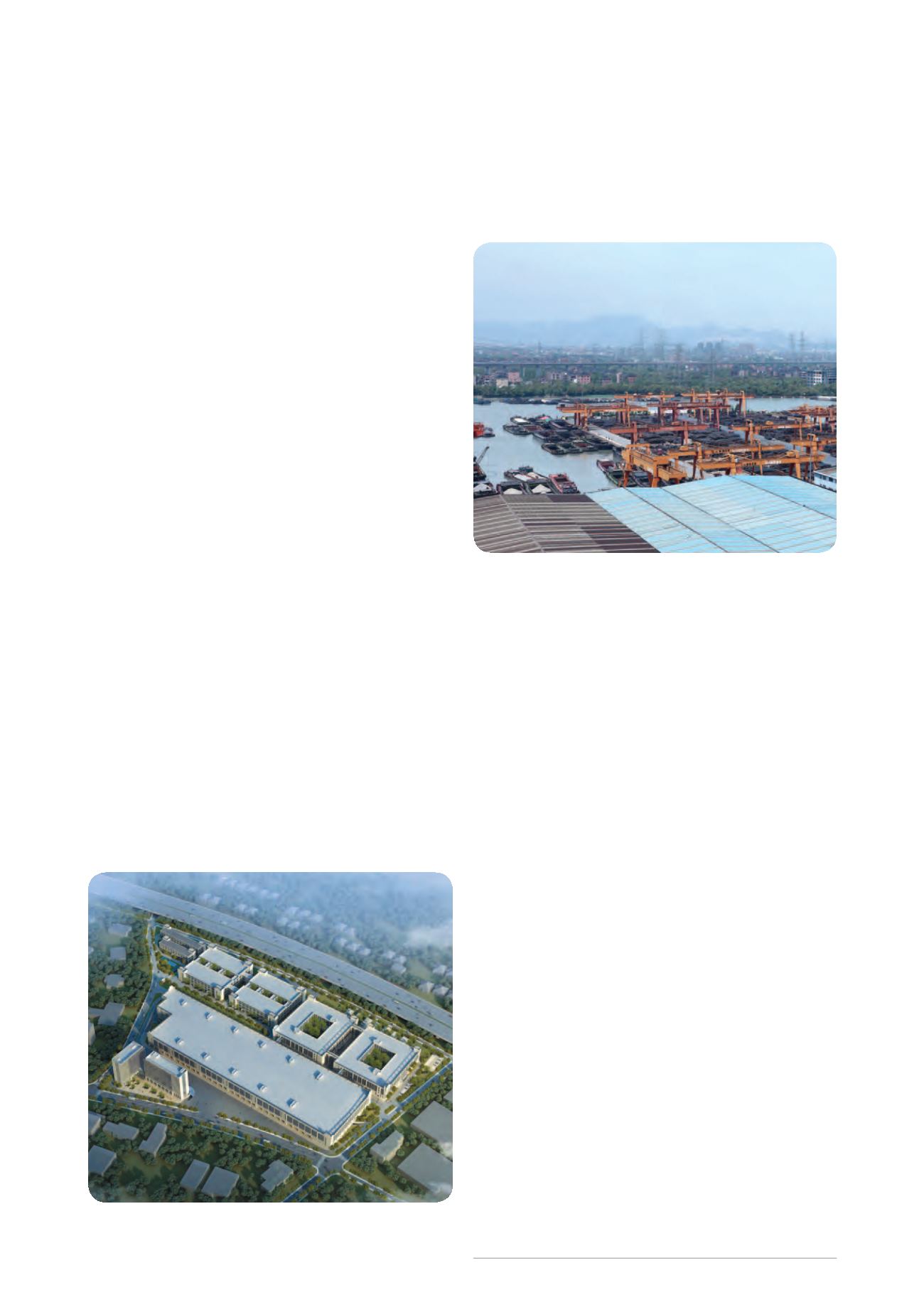

ECW was established as a private trust on 5 August

2015. A total of six properties was acquired between

25 August 2015 and 6 November 2015 (both dates

inclusive). ECW was officially listed on 28 July 2016 on the

SGX-ST Mainboard, backed by Forchn Holdings Group

Co., Ltd. (“the Sponsor”). The Sponsor, established in 1992,

is a diversified enterprise focusing on the industrial and

commercial real estate sectors, hospitality, e-commerce

logistics and finance.

For the period from 28 July 2016 to 31 December 2016,

ECW achieved a gross revenue of S$41.2 million and net

property income (“NPI”) of S$36.8 million, exceeding its

IPO forecast by 4.8% and 2.9% respectively. The better

performance was mainly due to the additional rental

income generated from asset enhancement initiatives

at Chongxian Port Investment (i.e. construction of a

sheltered warehouse) from 1 October 2016 as well as

favorable exchange rate movements.

Based on the distribution per unit of 2.454 cents for the

period from 28 July 2016 to 31 December 2016, the

annualised distribution yield for ECW is approximately

7.06% based on the IPO price of S$0.81.

Borrowings and aggregate leverage

At the Listing Date, ECW obtained a RMB1,004.2 million

(equivalent to S$209.0 million) Onshore secured floating

rate term loan facility, and a S$200.0 million syndicated

Offshore secured floating rate term loan facility. The

facilities were fully drawn at the Listing Date to finance

the acquisition of the properties. As at 31 December 2016,

the weighted average debt to maturity was 2.6 years while

the gearing ratio stood at 27.6%, which falls within the

Monetary Authority of Singapore’s leverage limit of 45%.

The Manager adopts a disciplined and prudent capital

management approach to maintain a strong capital

structure and financial flexibility. The Manager is working

actively with various financial institutions to achieve a

favourable debt maturity profile.

Risk management

The Manager undertakes a dynamic approach to

minimise the impact of foreign exchange and interest rate

volatilities on distributable income.

For the financial year ended 31 December 2016 (“FY2016”),

100.0% of ECW’s distributable income was being hedged

into Singapore dollars. About 24.4% of ECW’s total debt

was hedged into fixed rates through interest rate swaps

as at 31 December 2016.

Where feasible, after taking into account cost, tax and

other considerations, the Manager will borrow in the

same currency as the underlying assets to provide some

natural hedge, or hedge through cross currency swaps

for its cross border cash flows.

The fair value of the hedge instruments at the end of

FY2016, which were included as derivative financial

instruments in Total Assets and Total Liabilities, were

S$417,000 and S$387,000 respectively. The net derivative

financial asset represented 0.004% of the net assets of

ECW Group as at 31 December 2016.